Why Is PM Modi Encouraging Indians to Stop Buying Gold? (2026)

Why Is PM Modi Encouraging Indians to Stop Buying Gold? Gold has always held a special place in Indian households. For generations, families have invested in gold because of its cultural importance, emotional value, liquidity, and perception as a safe financial asset. However, in recent years, policymakers and financial experts have increasingly encouraged people to reduce excessive dependence on gold investments and focus more on productive assets that support long-term financial growth and economic development. The discussion around why Indians should stop buying gold excessively is not about eliminating gold entirely from investment portfolios. Instead, it is about encouraging balanced investment strategies that create stronger financial growth, economic productivity, and long-term wealth creation opportunities. At Nvedya Professionals LLP, financial awareness and smart investment planning are considered essential for helping individuals make informed and future-focused financial decisions. Why Gold Has Traditionally Been a Popular Investment Gold has historically been viewed as a symbol of financial security in India. During periods of inflation, uncertainty, or economic instability, many investors preferred gold because it was considered a reliable store of value. Some common reasons people invested heavily in gold include: Cultural and traditional importance Easy liquidity during emergencies Protection against inflation Long-term wealth preservation Emotional and family value For many years, gold remained one of the most trusted investment choices for Indian households. Why Experts Are Encouraging People to Stop Buying Gold Excessively Although gold remains an important asset, financial experts believe excessive investment in gold can limit wealth creation opportunities. Gold primarily acts as a passive store of value and does not actively contribute to economic productivity. When large amounts of money are invested only in gold, less capital flows into sectors that generate employment, infrastructure, business growth, and long-term economic expansion. This is one of the main reasons policymakers and economists encourage investors to diversify toward productive investment options such as: Real estate Equity investments Mutual funds Businesses and startups Infrastructure-driven assets Balanced investments often create better financial growth opportunities compared to relying heavily on a single traditional asset. How Excessive Gold Imports Affect the Economy India imports a large quantity of gold every year. Excessive gold imports increase pressure on foreign exchange reserves and can impact the country’s trade balance. When savings are directed mainly toward imported gold rather than productive sectors, economic growth opportunities may reduce because less money enters industries that create jobs and infrastructure. Financial experts often emphasize that investments in productive sectors support: Employment generation Business expansion Urban development Economic activity Infrastructure growth This broader economic perspective is an important reason behind discussions encouraging people to stop buying gold excessively.This is one of the reasons financial experts encourage investors to gradually stop buying gold excessively and focus on productive assets. Why Investment Diversification Is Important Modern financial planning focuses heavily on diversification. Instead of concentrating wealth in a single asset class, experts recommend balanced investment portfolios that combine stability with growth potential. A diversified investment strategy may include: Gold for safety and stability Mutual funds for long-term returns Real estate for appreciation and passive income Equity investments for wealth growth Fixed-income assets for financial security Diversification helps reduce financial risk while improving long-term wealth creation potential. At Nvedya Professionals LLP, structured financial planning focuses on helping individuals build balanced investment strategies aligned with their financial goals and risk profiles.Instead of relying completely on traditional assets, investors are now advised to stop buying gold excessively and adopt diversified financial planning strategies. Why Real Estate Is Emerging as a Preferred Investment Option As investors diversify beyond traditional gold-heavy portfolios, real estate is emerging as one of the most attractive long-term investment options. Unlike gold, real estate provides multiple financial advantages, including: Tangible asset ownership Rental income opportunities Long-term capital appreciation Inflation protection Portfolio diversification Infrastructure growth, urban expansion, and increasing housing demand are making property investment increasingly attractive in developing cities across India. Productive Assets Create Long-Term Wealth One of the biggest differences between gold and productive assets is their contribution to long-term economic activity and wealth generation. Investments in businesses, real estate, infrastructure, and financial markets actively contribute toward: Economic development Job creation Increased productivity Financial growth opportunities This is why modern investment strategies increasingly focus on assets that combine stability with long-term growth potential. Should Investors Completely Stop Buying Gold? Most financial experts do not recommend completely eliminating gold from an investment portfolio. Gold still plays an important role in diversification and financial security during uncertain market conditions. However, the key message behind discussions around stopping excessive gold purchases is the importance of balance. Investors should avoid concentrating most of their wealth in a single passive asset and instead adopt diversified financial strategies. (Stop Buying Gold) Smart financial planning focuses on combining safety, liquidity, growth, and long-term wealth creation across multiple asset classes. Importance of Financial Awareness in Modern Investing Today’s investment environment is changing rapidly. Rising inflation, evolving markets, infrastructure growth, and global economic shifts require more strategic financial planning than ever before. Financial awareness helps individuals: Understand investment risks Build diversified portfolios Improve long-term financial stability Make informed wealth-building decisions At Nvedya Professionals LLP, financial education and strategic advisory services aim to help individuals and businesses make smarter financial decisions for sustainable long-term growth. Conclusion The growing discussion around why Indians should stop buying gold excessively is connected to the broader importance of productive investments and balanced financial planning. While gold continues to hold cultural and financial significance, modern investment strategies increasingly emphasize diversification, economic productivity, and long-term wealth creation. By combining traditional assets like gold with growth-oriented investments such as real estate, mutual funds, and financial instruments, investors can create stronger and more sustainable financial futures. In today’s evolving economy, informed and balanced investment decisions are becoming more important than ever.The discussion around why Indians should stop buying gold excessively is mainly connected to diversification and productive financial growth. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

The Importance of Maintaining Proper Financial Records

The Importance of Maintaining Proper Financial Records Understanding Financial Records In today’s competitive business environment, maintaining proper financial records is essential for every organization, whether small or large. Accurate records help businesses track income, expenses, profits, taxes, and overall financial performance. Without proper documentation, managing business operations becomes difficult and risky. In simple terms, financial records are documents that contain information about a company’s financial transactions. These may include invoices, receipts, bank statements, tax filings, payroll details, and expense reports. Proper record management helps businesses stay organized and make informed decisions. Why Financial Records Are Important Maintaining accurate financial records helps businesses understand their financial position clearly. Business owners can track profits, monitor expenses, and identify areas where improvements are needed. Well-maintained records also reduce confusion and improve financial transparency. When financial information is organized properly, decision-making becomes easier. Businesses can plan budgets, manage investments, and control cash flow more effectively. Accurate records also help companies prepare for future growth opportunities. Better Financial Planning One major benefit of maintaining financial records is better financial planning. Businesses that regularly track their transactions can analyze spending patterns and manage resources efficiently. Financial planning becomes more effective when business owners have access to accurate data. They can estimate future expenses, set realistic goals, and prepare strategies for business expansion. Proper planning also helps companies avoid unnecessary financial stress. The Role of Financial Records in Tax Compliance Tax compliance is one of the most important reasons for maintaining proper financial documentation. Businesses are required to maintain records for GST filings, income tax returns, TDS, audits, and other legal requirements. Accurate financial records help businesses file taxes correctly and avoid penalties. During audits or government inspections, organized records provide proof of transactions and financial activities. This reduces the risk of legal complications and compliance issues. Avoiding Financial Errors Poor record management can lead to serious financial mistakes. Missing invoices, incorrect calculations, or unrecorded transactions can create confusion and financial losses. Maintaining proper financial records helps businesses identify errors quickly and ensure accuracy in accounting processes. It also improves internal control systems and reduces the chances of fraud or mismanagement. Improving Business Decision-Making Business growth depends heavily on informed decision-making. Accurate records provide valuable insights into company performance, customer payments, operational costs, and profitability. With proper financial records, businesses can make smarter decisions related to investments, hiring, pricing, and expansion. Reliable financial data also helps management evaluate risks and opportunities more effectively. Financial Records and Cash Flow Management Cash flow management is critical for business stability. Many businesses face difficulties not because they are unprofitable, but because they fail to manage cash flow properly. Maintaining updated financial information helps businesses monitor incoming and outgoing cash regularly. Proper records allow companies to track pending payments, manage expenses, and maintain healthy financial operations. Building Trust and Professionalism Maintaining proper documentation also improves a company’s credibility. Investors, banks, clients, and financial institutions often review business records before making important decisions. Well-organized financial records create trust and show professionalism. Businesses with transparent financial systems are more likely to receive funding, partnerships, and long-term business opportunities. Digital Accounting and Modern Record Management Technology has transformed the way businesses manage their finances. Digital accounting software and cloud-based systems make record management easier, faster, and more secure. Businesses can now store invoices, generate reports, monitor transactions, and maintain backups digitally. This improves efficiency and reduces paperwork-related errors. Modern tools also help businesses maintain financial records with greater accuracy and convenience. The Importance of Professional Financial Guidance Managing business finances requires knowledge, accuracy, and consistency. Many businesses struggle with accounting errors due to lack of expertise or poor documentation practices. Professional consultancy firms help businesses maintain organized records, manage taxation, and ensure compliance with financial regulations. Organizations like Nvedya Professionals LLP support businesses with accounting, taxation, compliance, and financial management solutions to improve operational efficiency. Small Businesses Need Proper Records Too Many small business owners believe financial management is only necessary for large companies. However, proper documentation is equally important for startups and small businesses. Maintaining accurate financial records from the beginning helps businesses grow systematically. It simplifies taxation, improves budgeting, and creates a strong foundation for future expansion. Conclusion Proper financial management is one of the most important factors behind business success. Maintaining organized and accurate financial information helps businesses improve planning, ensure compliance, manage cash flow, and make informed decisions. Financial records are the backbone of every successful business. Businesses that maintain transparency and proper documentation are better prepared for growth, stability, and long-term success. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

What Happens If You Don’t File ITR? Penalties & Risks Explained

What Happens If You Don’t File ITR? Penalties & Risks Explained Filing your Income Tax Return (ITR) is not just a legal obligation — it is a crucial part of maintaining financial transparency. However, many individuals still delay or completely ignore this responsibility. The consequences of Not Filing ITR can go beyond simple penalties and may affect your financial credibility in the long run. Understanding the risks of Not Filing (ITR) can help you make informed decisions and avoid unnecessary complications. Is Filing ITR Mandatory for Everyone? Not everyone is required to file ITR, but if your income exceeds the basic exemption limit or you meet certain criteria (like foreign travel or high-value transactions), filing becomes mandatory. Ignoring these conditions and continuing Not Filing ITR can lead to compliance issues with the Income Tax Department. Penalties for Not Filing ITR One of the most immediate consequences of Not Filing ITR is financial penalty. 1. Late Filing Fee (Section 234F) If you miss the due date, you may have to pay: Up to ₹5,000 (depending on delay) ₹1,000 for small taxpayers This penalty applies even if you have no tax liability, making Not Filing ITR an unnecessary financial burden. 2. Interest on Tax Due (Section 234A) If you have unpaid taxes, interest is charged on the outstanding amount. This increases the overall liability when you continue Not Filing ITR. Legal Risks and Notices The Income Tax Department actively monitors financial transactions. Not Filing ITR can trigger notices, especially if your financial activities are recorded through PAN-linked systems. Possible Consequences: Receiving income tax notices Scrutiny of your financial records Reassessment of income Ignoring compliance repeatedly can even lead to legal action in severe cases. Loss of Financial Benefits Many people underestimate how Not Filing ITR affects financial opportunities. 1. Difficulty in Getting Loans Banks often require ITR as proof of income. Without it, loan approvals may be delayed or rejected. 2. Visa and Travel Issues ITR documents are often required for visa applications. Not Filing ITR can create hurdles in international travel plans. 3. No Carry Forward of Losses If you incur losses (like in stocks or business), you cannot carry them forward unless you file your ITR on time. Impact on Financial Reputation Consistent Not Filing ITR can affect your financial credibility. Whether you are an individual or a business owner, maintaining proper tax records builds trust with financial institutions and authorities. A poor compliance record may raise red flags in future financial dealings. Common Reasons People Avoid Filing ITR Understanding why people delay helps address the issue: Lack of awareness Fear of complex procedures Assumption of no tax liability Procrastination However, these reasons do not justify Not Filing ITR, especially when the consequences are significant. How to Stay Compliant Avoiding the risks of Not Filing ITR is simple if you follow a structured approach: Keep all financial records organized Track income and deductions File returns before the due date Verify your return after filing Stay updated with tax rules Taking these steps ensures smooth compliance and avoids penalties. When Should You Seek Professional Help? If your income sources are multiple, involve business transactions, or include investments, it is advisable to consult professionals. Working with experts like Nvedya Professionals LLP can simplify the entire process. From accurate filing to proper tax planning, professional guidance ensures that you remain compliant and stress-free. Final Thoughts Not filing your ITR may seem like a small delay, but it can lead to penalties, notices, and long-term financial consequences. The risks of Not Filing ITR are avoidable with timely action and proper awareness. Filing your return on time not only keeps you compliant but also strengthens your financial profile. With the right approach and expert support when needed, you can manage your tax responsibilities efficiently and avoid unnecessary complications. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

Income Tax Notices India: What They Mean and How to Respond Safely

Income Tax Notices India: What They Mean and How to Respond Safely Receiving a notice from the Income Tax Department can be stressful, especially if you are unsure about the reason behind it. However, not all notices indicate a problem. Understanding Income Tax Notices India can help you respond calmly and correctly without unnecessary panic. In many cases, these notices are simply requests for clarification or additional information. Knowing how Income Tax Notices India work is essential for every taxpayer. What Are Income Tax Notices? Income tax notices are official communications sent by the Income Tax Department to taxpayers. These notices may be issued for various reasons such as discrepancies in income, missing information, or verification requirements. Understanding the purpose of Income Tax Notices India helps you take the right steps without delay. Common Reasons for Receiving a Notice There are several reasons why taxpayers receive Income Tax Notices India, including: Mismatch between declared income and reported transactions Failure to file income tax returns High-value transactions flagged by the system Incorrect claims for deductions Random scrutiny or verification These reasons do not always indicate wrongdoing but require timely attention. Types of Income Tax Notices in India 1. Notice Under Section 139(9) Issued when your return is considered defective due to errors or missing details. 2. Notice Under Section 142(1) Sent to request additional documents or information. 3. Notice Under Section 143(1) An intimation notice highlighting calculation differences. 4. Notice Under Section 143(2) Issued when your return is selected for detailed scrutiny. 5. Notice Under Section 148 Sent when the department believes income has escaped assessment. Understanding these types of Income Tax Notices India helps you identify the seriousness of the situation. How to Respond Safely to Income Tax Notices Handling Income Tax Notices India properly is crucial to avoid penalties or legal complications. Follow these steps: 1. Stay Calm and Read Carefully Do not panic. Carefully read the notice to understand its purpose and deadline. 2. Verify the Authenticity Always check whether the notice is genuine by logging into the official income tax portal. 3. Gather Required Documents Collect all necessary documents such as bank statements, invoices, and previous returns. 4. Respond Within Deadline Timely response is critical. Ignoring Income Tax Notices India can lead to penalties. 5. Seek Professional Help If the notice is complex, consult experts for accurate response and compliance. Common Mistakes to Avoid Many taxpayers make errors while handling Income Tax Notices India, which can worsen the situation: Ignoring the notice Missing deadlines Providing incorrect or incomplete information Responding without proper understanding Not maintaining documentation Avoiding these mistakes ensures smooth resolution. When Should You Take Expert Help? Not all notices require professional intervention, but in cases involving scrutiny, reassessment, or large financial discrepancies, expert guidance is highly recommended. Working with professionals like Nvedya Professionals LLP ensures that your response is accurate, compliant, and stress-free. Experts can help you interpret Income Tax Notices India, prepare documentation, and communicate effectively with authorities. Why Timely Response Matters Ignoring Income Tax Notices India can lead to penalties, legal action, or additional scrutiny. On the other hand, a timely and accurate response can resolve the issue quickly and maintain your compliance record. Being proactive not only saves money but also builds credibility as a responsible taxpayer. Final Thoughts Receiving a tax notice is not something to fear — it is a part of the compliance system designed to ensure transparency and accuracy. The key lies in understanding the notice, responding within timelines, and maintaining proper documentation. At the same time, handling such matters without clarity can lead to unnecessary stress or mistakes. Having the right guidance can make the process much simpler and more efficient. Professional support from firms like Nvedya Professionals LLP can help you interpret notices correctly, respond with confidence, and stay fully compliant without complications. In the end, being informed and prepared is what truly matters. With the right approach and expert support when needed, you can handle tax notices smoothly and focus on your financial growth with peace of mind. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

Hidden Compliance Costs of Running a Startup in India

Hidden Compliance Costs of Running a Startup in India (What Founders Must Know) Starting a business in India involves more than just an idea, funding, and execution. Many founders underestimate the Hidden Compliance Costs associated with running a startup. These costs often go unnoticed during the planning stage but can significantly impact cash flow and long-term sustainability. Understanding these Hidden Compliance Costs is essential for building a financially stable business and avoiding unexpected financial stress. Why Compliance Costs Are Often Overlooked Most entrepreneurs focus on visible expenses such as office setup, salaries, and marketing. However, Hidden Compliance Costs are not always clearly communicated or understood in the early stages. These costs arise from legal requirements, tax regulations, and ongoing filings that every business must follow. Ignoring these Compliance Costs can lead to penalties, operational disruptions, and reputational risks Major Hidden Compliance Costs Startups Face 1. Business Registration and Setup Charges While registering a company may seem straightforward, there are multiple associated expenses that fall under Hidden Compliance Costs. These include professional fees, documentation charges, government fees, and digital signature costs. Tip: Plan a detailed budget for registration instead of assuming minimal expenses. 2. Accounting and Bookkeeping Expenses Maintaining proper financial records is mandatory, yet many founders ignore this aspect initially. Over time, bookkeeping becomes one of the recurring Hidden Compliance Costs. Tip: Invest in accounting tools or professional services early to avoid errors and penalties. 3. GST Compliance and Filing Costs GST registration may be free, but regular filing, reconciliation, and compliance create ongoing Hidden Compliance Costs. Late filings can result in penalties, increasing the financial burden. Tip: Ensure timely GST filings and maintain accurate transaction records. 4. ROC and Annual Filing Fees Companies registered in India must file annual returns with regulatory authorities. These filings contribute significantly to Hidden Compliance Costs. Tip: Track compliance deadlines and allocate a yearly budget for filings. 5. Legal Documentation and Agreements Drafting contracts for co-founders, employees, and vendors is essential but often ignored. Legal documentation adds to Hidden Compliance Costs, especially when done later in urgency. Tip: Create structured agreements from the beginning to avoid disputes and higher costs later. 6. Professional Consultation Fees Seeking expert advice for taxation, compliance, and financial planning is crucial. However, many startups consider this an optional expense, not realizing it is part of Hidden Compliance Costs. Tip: Treat professional guidance as an investment rather than an expense. 7. Penalties Due to Non-Compliance One of the most avoidable yet common Hidden Compliance Costs comes from penalties and late fees. Missed deadlines, incorrect filings, or lack of compliance awareness can lead to significant financial losses. Tip: Stay proactive and maintain a compliance calendar. How to Manage Hidden Compliance Costs Effectively Managing Hidden Compliance Costs requires planning and awareness. Start by identifying all possible compliance requirements applicable to your business. Create a budget that includes both fixed and variable compliance expenses. Using technology and automation tools can also help reduce manual errors and costs. Working with experts like Nvedya Professionals LLP ensures that your startup stays compliant while optimizing costs. Professional guidance helps in identifying potential risks and minimizing unnecessary expenses. Why Planning These Costs is Crucial Ignoring Hidden Compliance Costs can disrupt your financial planning and reduce profitability. Startups often fail not because of lack of revenue, but because of poor cost management. When you plan these costs in advance, you gain better control over your finances and can make informed business decisions. Final Thoughts Running a startup successfully requires more than just innovation and execution. It demands awareness of every financial aspect, including Hidden Compliance Costs that are often overlooked. By understanding these expenses, planning ahead, and seeking expert support, entrepreneurs can avoid unnecessary stress and focus on growth. The key is not just to start a business, but to sustain it with strong financial and compliance foundations. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

Top 7 Legal & Tax Mistakes Startups Make in India (And How to Avoid Them)

Top 7 Legal & Tax Mistakes Startups Make in India (And How to Avoid Them) Starting a business in India is exciting, but it also comes with responsibilities that many founders underestimate. One of the biggest reasons startups struggle is due to Legal & Tax Mistakes Startups make in their early stages. These mistakes may seem minor initially, but they can lead to penalties, compliance issues, and financial losses over time. Understanding the common Legal & Tax Mistakes Startups make can help entrepreneurs build a strong foundation and avoid unnecessary risks. Why Legal & Tax Planning Matters for Startups Most founders focus on growth, marketing, and product development, often ignoring compliance. However, Legal & Tax Mistakes Startups make can directly impact credibility and sustainability. Strong legal and tax planning ensures smooth operations, helps in building investor confidence, and protects your business from regulatory challenges. Avoiding Legal & Tax Mistakes Startups commonly face should be a priority from day one. Top 7 Legal & Tax Mistakes Startups Make 1. Choosing the Wrong Business Structure Selecting the wrong business structure is one of the most common Legal tax mistakes startups make. Many founders choose based on convenience rather than long-term goals. How to Avoid: Evaluate options like Proprietorship, LLP, or Private Limited Company based on scalability, funding needs, and tax implications. 2. Ignoring GST Registration Delaying GST registration is another frequent legal and tax mistake startups make. This can lead to penalties and business restrictions. How to Avoid: Register for GST on time if your turnover crosses the threshold or if your business model requires it. 3. Poor Bookkeeping Practices Improper financial record-keeping is among the most damaging legal and tax mistakes startups commit. How to Avoid: Maintain accurate books of accounts using accounting tools or professional services from the beginning. 4. Mixing Personal and Business Finances Many founders mix personal and business expenses, which is a serious Legal & Tax Mistakes Startups often overlook. How to Avoid: Keep a separate business bank account and clearly track all transactions. 5. Missing Tax Deadlines Late filing of returns is one of the costliest Legal & Tax Mistakes Startups make, leading to penalties and interest. How to Avoid: Track all compliance deadlines and ensure timely filings. 6. Lack of Legal Agreements Skipping contracts is another major Legal & Tax Mistakes Startups make, especially in early collaborations. How to Avoid: Prepare proper agreements for co-founders, employees, and vendors to avoid disputes. 7. Not Taking Professional Advice Trying to manage compliance without expert help results in multiple legal and tax mistakes. Startups could easily avoid. How to Avoid: Seek professional guidance for taxation, compliance, and financial planning. How to Avoid These Mistakes To prevent Legal Tax Mistakes Startups make; founders should adopt a proactive approach. Start by planning compliance early, staying updated with regulations, and maintaining proper documentation. Working with experts like Nvedya Professionals LLP can simplify complex processes. From registrations to tax filings, professional support helps reduce risks and ensures smooth business operations. Final Thoughts Many startups fail not because of poor ideas, but due to avoidable compliance errors. The most critical challenges often arise from Legal & Tax Mistakes Startups ignore in the beginning. By focusing on proper planning, maintaining financial discipline, and taking expert advice, entrepreneurs can build a strong and sustainable business. Avoiding these mistakes is not just about compliance — it is about creating a solid foundation for long-term success. Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

Right Time to Start a Business: Bengaluru CA Explains the Biggest Entrepreneur Trap

Right Time to Start a Business: Bengaluru CA Explains the Biggest Entrepreneur Trap Starting a business is a dream for many, but very few succeed in turning that dream into reality. One of the biggest reasons behind failure is not a lack of ideas or funding—it is misunderstanding the right time to start a business. A Bengaluru-based chartered accountant highlights that most entrepreneurs fall into a common trap related to timing. Knowing when to launch is the make-or-break factor of a successful business. Most people either skip on actually launching or put it off forever because perfect conditions never arrive. Both of them can be just as harmful. What is the timing trap in business? The timing trap refers to the confusion around identifying the right time to start a business. Entrepreneurs often make one of two mistakes. First, they start too early. In this case, they lack proper planning, financial clarity, and market understanding. Without these essentials, even a strong idea may fail. Second, they start too late. They keep waiting for better opportunities, more savings, or perfect knowledge. This delay often leads to missed opportunities, making them lose the right time to start a business. Why the Right Time to Start a Business Matters Choosing the right time to start a business is critical because it impacts market entry, competition, and growth potential. If you enter too early, the market may not be ready. If you enter too late, competitors may dominate. The right time to start a business ensures that you balance preparation with action. It allows you to enter the market with confidence while still being flexible to adapt. Signs You Have Found the Right Time to Start Business Instead of waiting for perfection, you should look for clear indicators that suggest the right time to start a business has arrived. You have a clear and validated business idea You understand your target audience You have basic financial planning in place You are mentally prepared for risks You have some financial backup or support When these elements align, it often indicates the right time to start a business. Common Mistakes While Deciding the Right Time Many entrepreneurs fail because they misjudge the right time to start a business. Here are common mistakes: Overthinking: Waiting endlessly for perfect timing Overconfidence: Starting without research Ignoring finances: Lack of budgeting and planning Skipping legal compliance: Not consulting professionals Fear of failure: Avoiding action completely Avoiding these mistakes can help you identify the right time to start business more effectively. How to Identify the Right Time to Start a Business There is no universal formula, but you can evaluate three key factors to determine the right time. 1. Personal Readiness Your skills, experience, and mindset play a major role. If you are ready to handle uncertainty, it may be the right time to start a business. 2. Financial Stability You don’t need huge capital, but you should have enough funds to sustain operations. Financial readiness strongly indicates the right time. 3. Market Opportunity If there is demand for your product or service, it could be the right time. Market gaps create opportunities for growth. Expert Advice from Bengaluru CA According to the CA, instead of chasing the perfect moment, focus on preparing yourself. The right time to start a business is when preparation meets opportunity. He suggests: Start small but think long-term Validate your idea before investing heavily Take professional advice for compliance and taxation Focus on learning and improvement These steps help ensure that you don’t miss the right time to start a business. Final Thoughts Entrepreneurship is not about waiting endlessly for the perfect moment, nor is it about rushing in without preparation. The real success lies in finding the balance between readiness and action. When your idea is validated, your fundamentals are clear, and you are mentally prepared to take calculated risks — that is your signal to begin. At the same time, one aspect that many aspiring entrepreneurs overlook is the importance of proper financial planning, compliance, and structured guidance in the early stages. Ignoring these can lead to challenges that slow down growth or create unnecessary risks. This is where professional support becomes valuable. Firms like Nvedya Professionals LLP help entrepreneurs navigate the complexities of starting and managing a business — from registrations and taxation to strategic financial planning. With the right guidance, founders can avoid common mistakes and focus more on building and scaling their vision. In the end, success is not about perfect timing — it is about making informed decisions, staying consistent, and having the right support system in place. When preparation meets the right execution, growth naturally follows. 🚀 Media Contact Nvedya Professionals LLP 📧 Email: contact@nvedya.in 🌐 Website: www.nvedya.in Follow us on: Facebook | Instagram | LinkedIn

Financial Year-End Checklist for Businesses in India (2026 Guide)

📝 Financial Year-End Checklist for Businesses in India (2026 Guide) As the financial year comes to a close, businesses across India enter a crucial phase of reviewing, reconciling, and preparing their financial records. A structured financial year-end checklist helps ensure that all accounting entries are accurate, tax obligations are fulfilled, and compliance requirements are met without last-minute stress. Whether you are running a startup, a small business, or a growing enterprise, following a systematic approach at year-end can save you from penalties, improve financial clarity, and support better decision-making for the upcoming year. 📊 Importance of Year-End Financial Planning A well-organized financial year-end checklist is not just about closing books; it is about setting a strong financial foundation for the future. Businesses that actively review their finances at the end of the year are better prepared for audits, tax filings, and strategic planning. It helps identify discrepancies, ensures that all income and expenses are properly recorded, and gives a clear picture of the company’s financial health. Ignoring this process can lead to compliance issues, incorrect tax calculations, and missed opportunities for savings. 🧾 Reviewing Financial Records One of the first steps in any financial year-end checklist is to carefully review all financial statements. This includes verifying the profit and loss statement, balance sheet, and cash flow records. Every transaction should be checked to ensure it is correctly recorded and categorized. This process helps in identifying errors, duplicate entries, or missing transactions that may affect the final financial reports. Accurate financial records are essential not only for compliance but also for making informed business decisions. 💰 Bank Reconciliation and Cash Flow Check Another important aspect of the financial year-end checklist is reconciling bank accounts. Businesses should match their internal records with bank statements to ensure that all transactions are accounted for. Any discrepancies, such as unrecorded payments or incorrect entries, should be resolved immediately. Along with reconciliation, reviewing cash flow is equally important. Understanding how money is moving in and out of the business helps in planning expenses, managing liquidity, and avoiding financial bottlenecks in the next financial year. 📉 Managing Receivables and Payables A comprehensive financial year-end checklist also involves evaluating accounts receivable and payable. Businesses should follow up on pending payments from customers and clear outstanding dues to suppliers. This step not only improves cash flow but also strengthens business relationships. In some cases, bad debts may need to be written off to reflect a realistic financial position. Proper management of receivables and payables ensures that financial statements present an accurate picture of the company’s obligations and earnings. 🧾 GST and Tax Compliance Tax compliance plays a major role in the financial year-end checklist for businesses in India. It is essential to reconcile GST returns, ensuring that GSTR-1 matches with GSTR-3B and that input tax credit is correctly claimed. Any pending GST filings should be completed before deadlines to avoid penalties. Additionally, businesses must review their TDS obligations, ensure timely filing of returns, and verify that advance tax payments are made where applicable. Proper tax planning at this stage can help reduce liabilities and prevent compliance issues. 🏢 Asset and Inventory Verification Verifying assets and inventory is another critical component of the financial year-end checklist. Businesses should physically check their fixed assets and update the asset register accordingly. Depreciation must be calculated accurately as per applicable rules. For companies dealing with goods, conducting a stock audit is essential to identify damaged, obsolete, or slow-moving inventory. This step ensures that financial statements reflect the correct valuation of assets and inventory, which is crucial for both taxation and reporting purposes. 📑 Preparing for Income Tax Filing As the year ends, businesses must start preparing for income tax filing as part of their financial year-end checklist. This includes organizing all financial documents, calculating taxable income, and identifying eligible deductions. Early preparation reduces the risk of errors and allows sufficient time to plan taxes efficiently. Businesses that delay this process often face last-minute pressure, which can lead to mistakes and penalties. ⚠️ Common Mistakes to Avoid While completing the financial year-end checklist, many businesses make avoidable mistakes such as skipping reconciliation, missing compliance deadlines, or maintaining incomplete documentation. These errors can result in financial discrepancies and legal complications. It is important to stay proactive, maintain proper records, and seek professional guidance when needed to ensure smooth year-end closure. 🎯 Conclusion A well-executed financial year-end checklist is essential for maintaining financial discipline, ensuring compliance, and preparing your business for future growth. By reviewing records, managing taxes, and verifying assets, businesses can close their financial year with confidence and clarity. Proper planning and timely action not only reduce risks but also create opportunities for better financial management in the coming year. Media Contact Nvedya Professionals LLPEmail: contact@nvedya.inWebsite: www.nvedya.inFollow us on: Facebook | Instagram | LinkedIn

Startup Tax Benefits in India You Should Not Miss (2026 Guide)

🏆 Startup Tax Benefits in India You Should Not Miss (2026 Guide) Starting a business in India is an exciting journey, but managing finances and taxes can be challenging. The good news is that the government offers several startup tax benefits to encourage innovation, entrepreneurship, and economic growth. If you are a startup founder or planning to launch your venture, understanding these startup tax benefits can help you save a significant amount of money legally while boosting your business growth. In this guide, we will explain the most important tax benefits in India that you should not miss in 2026. 💡 What Qualifies as a Startup in India? Before claiming any startup tax benefits, your business must be recognized as a startup by DPIIT (Department for Promotion of Industry and Internal Trade). ✔️ Eligibility Criteria: Company age should be less than 10 years Annual turnover should not exceed ₹100 crore Must be working towards innovation or improvement Should not be formed by splitting an existing business Once recognized, your business becomes eligible for multiple tax benefits. 🏅 1. Tax Holiday Under Section 80-IAC One of the most powerful startup tax benefits in India is the tax holiday under Section 80-IAC. 📌 Key Benefits: 100% tax exemption on profits Available for any 3 consecutive years out of 10 years Applicable only to DPIIT-recognized startups This is a major advantage as it allows startups to reinvest profits into growth without worrying about taxes. 💸 2. Angel Tax Exemption Startups often raise funds from investors, and earlier, this attracted angel tax. However, now eligible startups can enjoy this important startup tax benefits. 📌 Highlights: Exemption from angel tax under Section 56 Applicable on investments above fair market value Helps attract investors without tax burden This startup tax benefits is crucial for early-stage funding. 📉 3. Carry Forward of Losses Another valuable startup tax benefits is the ability to carry forward losses. 📌 Key Points: Losses can be carried forward for up to 8 years Helps reduce future taxable income Shareholding condition relaxed for startups This ensures startups can stabilize financially in initial years. 🧾 4. GST Benefits for Startups GST compliance can be complex, but certain tax benefits simplify it. 📌 Advantages: Composition scheme for small businesses Lower compliance burden Input tax credit benefits Proper GST planning can significantly improve cash flow. 🏢 5. Capital Gains Tax Exemption Startups can also enjoy startup tax benefits on capital gains under certain conditions. 📌 Key Sections: Section 54GB – Exemption on capital gains invested in startups Section 54EE – Investment in specified funds This encourages investment into the startup ecosystem. 📊 6. Presumptive Taxation for Small Startups Small startups and professionals can opt for presumptive taxation schemes. 📌 Benefits: Reduced compliance Fixed percentage taxation No need for detailed bookkeeping This is one of the most practical startup tax benefits for small businesses. ⚠️ Common Mistakes to Avoid Even with multiple startup tax benefits, many founders make mistakes: ❌ Not registering under DPIIT ❌ Missing compliance deadlines ❌ Improper documentation ❌ Ignoring professional advice Avoiding these ensures you fully utilize all startup tax benefits. 📅 Latest Updates in 2026 Extended eligibility for startup recognition Simplified tax compliance procedures Increased support for innovation-driven startups Staying updated helps maximize your startup tax benefits 🎯 Conclusion Understanding and utilizing startup tax benefits in India can make a huge difference in your business journey. From tax holidays to investor-friendly policies, these benefits are designed to support your growth. If you plan strategically, you can legally reduce your tax burden and reinvest more into scaling your startup. Media Contact Nvedya Professionals LLPEmail: contact@nvedya.inWebsite: www.nvedya.inFollow us on: Facebook | Instagram | LinkedIn

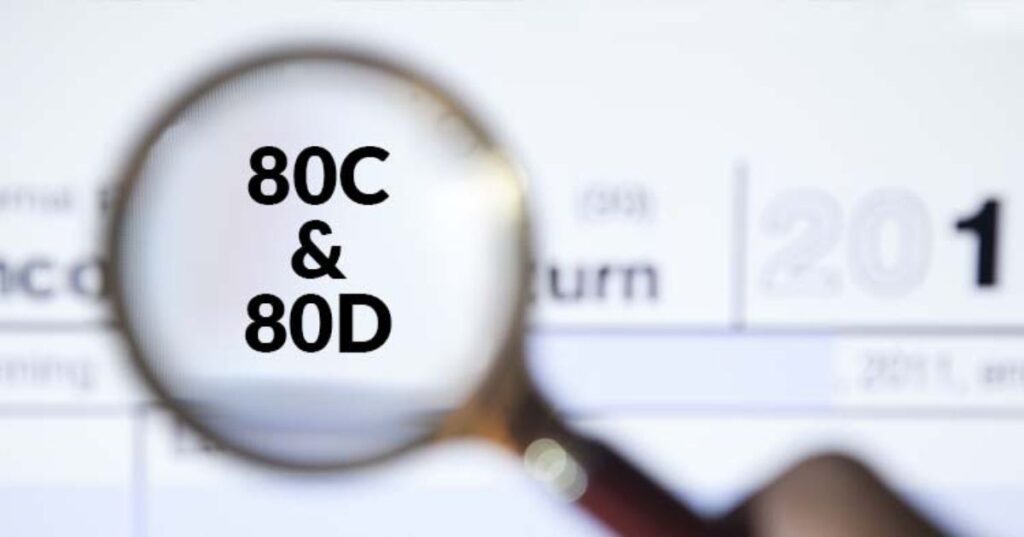

Section 80C to 80D Explained: Complete Tax Saving Guide for 2026

Section 80C to 80D Explained: Complete Tax Saving Guide for 2026 Understanding tax-saving options is essential for every taxpayer in India. With rising income levels and evolving tax regulations, knowing where and how to save tax can make a significant difference in your financial planning. This guide on Section 80C to 80D Explained will help you understand the most important deductions available under the Income Tax Act. From investments to insurance, these sections offer multiple ways to reduce your taxable income legally. What is Section 80C? When we talk about Section 80C to 80D Explained, Section 80C is the most widely used tax-saving provision. It allows deductions of up to ₹1.5 lakh in a financial year. 🔹 Key Investments Under Section 80C: Public Provident Fund (PPF) Employee Provident Fund (EPF) Life Insurance Premium Equity Linked Saving Scheme (ELSS) Tax-saving Fixed Deposits Home Loan Principal Repayment These options not only help in tax saving but also build long-term wealth. In any discussion about Section 80C to 80D Explained, this section plays a crucial role for salaried individuals. What is Section 80D? Another important part of Section 80C to 80D Explained is Section 80D, which focuses on health insurance. 🔹 Deductions Under Section 80D: ₹25,000 for self and family ₹25,000 for parents (₹50,000 if senior citizens) Preventive health check-up included Health insurance not only protects you financially but also gives tax benefits. Understanding this part of Section 80C to 80D Explained ensures you don’t miss out on valuable deductions. Key Difference Between Section 80C and 80D While both sections help reduce taxes, they serve different purposes. Section Purpose Limit 80C Investments & savings ₹1.5 lakh 80D Health insurance ₹25,000–₹75,000 In this Section 80C to 80D Explained guide, it is important to understand that combining both sections can significantly reduce your taxable income. How to Maximize Tax Savings To make the most of Section 80C to 80D Explained, you should plan strategically: ✔ Use Full Limit of 80C Invest in a mix of safe and growth-oriented instruments. ✔ Don’t Ignore Health Insurance Section 80D benefits are often underutilized. ✔ Plan Early Avoid last-minute investments just to save tax. ✔ Combine Both Sections Using both sections together increases total deductions. Proper planning using Section 80C to 80D Explained strategies can help you save a substantial amount every year. Common Mistakes to Avoid Even after understanding Section 80C to 80D Explained, many taxpayers make mistakes: Investing without planning Ignoring medical insurance Not keeping proper documentation Missing deduction limits Avoiding these errors ensures smoother tax filing and maximum benefits. Why This Matters for Taxpayers in 2026 With increasing financial awareness, taxpayers are now focusing more on structured tax planning. This is where Section 80C to 80D Explained becomes highly relevant. It helps: Reduce taxable income Improve financial discipline Ensure future security Whether you are salaried or self-employed, understanding these deductions is crucial. FAQs Q1. What is the maximum deduction under Section 80C? Up to ₹1.5 lakh per financial year. Q2. Can I claim both 80C and 80D together? Yes, both can be claimed simultaneously for maximum tax savings. Q3. Is health check-up included under 80D? Yes, preventive health check-ups are covered. Q4. Why is Section 80C to 80D Explained important? It helps taxpayers understand how to legally reduce tax liability. Conclusion In conclusion, Section 80C to 80D Explained provides a complete roadmap for tax saving in India. By using the right combination of investments and insurance, you can reduce your tax burden while securing your financial future. 👉 Need expert help with tax planning? Connect with Nvedya Professionals for personalized tax-saving strategies and hassle-free compliance. Media Contact Nvedya Professionals LLPEmail: contact@nvedya.inWebsite: www.nvedya.inFollow us on: Facebook | Instagram | LinkedIn